Control Restaurant Expenses. Common Myths About Restaurant Costs Debunked

March 6, 2020 • 12 minutes

The proficiency required to understand and control expenses is not as simple as it may seem. Revenue and expense, purchasing and inventory management, profit and loss, and many other factors are all tied together with an enduring management oversight behavior supported by knowledge and understanding of the industry.

Becoming stagnant or comfortable in this arena is a dangerous cloud to hang over you. To help your restaurant management team cope with this challenge, we invited Jim Lopolito, President of a New York based restaurant consulting company, to share his knowledge on our blog.

If you’d like to establish control over your restaurant operating expenses, read on, and use Jim’s tips to know where your numbers are going before you get there.

Cloud POS for restaurants

Use Poster to make sales faster, manage your inventory and finances.

Control over restaurant expenses is a perceived outcome

We all know that the controlling of restaurant monthly expenses is a mix of: observing daily activities, market price research, purchasing effectiveness, having cost control procedures in place, effective use of restaurant POS system reports, and many other factors. However, at the heart of this idea, there is a misunderstood and almost impossible ability to achieve the goal of full control.

The control of restaurant costs is a delusional byproduct from the sanities of management in their perceived ability to perform this function. What this means is relatively straightforward. If you believe you have a handle on your restaurant expenses, you may actually not.

In fact, you won’t have a full understanding in controlling expenses without the consideration and inclusion of what is not in your control. Let’s illustrate this idea with an example related to restaurant menu pricing srategies that are influenced by costs of ingredients in the market.

In theory, you could try to control fluctuation in market costs through adjusting each affected recipe cost and corresponding menu price as they occur. While this solution offers balance on profit concerns, imagine how your customers would feel if you changed menu prices every time your costs changed. On top of that, even if you actually do this, your attempt is skewed and diluted because your menu sales mix changes every day.

In understanding different categories of expenses you must determine what you cannot control. Then, do your best with processes and procedures toward what you do have control over. This is important because there are restaurant operating costs that are out of your control, and if you are not aware of how this impacts upon your business, you may be misinterpreting your reporting.

For instance, your menu is a fixed piece of business material that doesn’t change every day. Let’s assume that today you can purchase fish for $5 a pound and you decide to set a $15 menu price for this item. You’ll expect 33% food cost based on only these two factors. Tomorrow the same fish can cost you $6 a pound and you’ll have a 40% food cost, but you do not change your menu price so you’ll be losing 7% for each sale in this transaction because the original pricing for the menu was based on the $5 per pound. Do you monitor such cases and account for this loss in your reports?

You might just follow a pattern that often occurs in the industry where you tell the chef that they have to do a better job in lowering the food cost. Oftentimes, this is difficult because the chef is ordering what is on the menu, and does not control market prices.

Non-controllable restaurant costs breakdown and ways to cope with them

You can only do your best to control costs that are within your ability, but in the end, the total control is really out of your hands. Let’s look at some common non-controllable expenses.

Daily vendor pricing fluctuations

The price and product from vendors changes regularly. These fluctuations can change average operating costs for a restaurant. You can try to minimize their influence by regulating how much you order and from which vendor. However, if you have to purchase the product because it is on your menu anyway, you have no choice over the price. In addition, you may have to select products based on quality or counts, which also affects your final costs.

Track purchase price fluctuations on all products as a variance report. This can be performed during inventory procedures, whereas, FIFO accounting can be used to offer a variance of amounts ordered against price differences during the month. The differences in month to month price variations can assist with decisions to adjust recipe costs and menu prices.

Daily menu mix

Even with suggestive selling, the overall selection process is by the guest. This selection in turn moves the outcome of your profit and loss for the day. The daily menu mix also affects other factors like usage and spoilage. You can maintain some control through effective ordering procedures, selling techniques, preparation methods, and economic product usage. However, purchasing and preparing the exact amounts of food to control these factors is extremely difficult.

Each day will offer a different revenue and profit outcome, and one reason for this is because you do not sell the same amounts of the same items every day. If you know the differences in profit from each item (known as contribution margin), you can track your efficiency and use this to train staff on selling the higher profit items.

Daily loss of product

While everyone tries to control breakage, loss of product, drops on the floor, spoilage, theft, and other similar loss of product factors, the control of these costs is essentially fate. Security of product can assist with some of these values; however, the best you can do is to be careful and proactive in addressing these circumstances and to record their value on profits.

You must track breakage, loss of product, drops on the floor, spoilage, theft, and other similar loss. You may be surprised at how these add up to loss of profits, and you should document this information in your reports.

Daily returns and adjustments

The control on returns and adjustments is basically in the hands of your guests. You can do your best to put out a good product, but not everyone is going to like what you produce. There are many factors like: returns, misfires, free meals provided by employees, or spillage. Those are examples of additional expenses that are not controlled by the business. Recoding them is the only way for you to know how they affect your profits.

Each item on the menu should have a recipe and cost. End of day reports should include; voids, comps, discounts, refunds, and any other information that you need to calculate additional expenses for the day. Every item should have a cost factor attached to it and you should track the amount you lost in revenue as a result of the lost product. If you comp a drink with a cost of $2, you didn’t just lose the $2. You also lose the difference in revenue from the lost sale from what you comp.

Laws affecting costs

Admit that no business can control the wage laws that have been affecting businesses. This is just one area of government control where you have no control. Taxes, labor laws, and other factors must all be considered. You can try everything in your power to reduce these costs, but in the end, you’ll have to fill every position in your restaurant to get the job done and pay the price set by the government.

No business can control the new wage laws and you can only do your best to adjust how you perform operational practices to achieve your best performance.

Now that you have recognized non-controllable expenses in restaurant business how can we use this to your advantage? Know that they exist and have a percentage or dollar adjustment allocated within reports based on your history.

Controllable restaurant expenses breakdown and ways to minimize them

Your restaurant controllable expenses require you to have a practice in place to regulate the outcome of your processes. Proactive procedures help with outcomes ahead, whereas, reactive procedures leave you behind. Without effective procedures and monitoring your outcome becomes ambiguous. Without conscious knowledge-based management you are just reacting to what happens to you and have minimum ability to influence your results.

Consider integrating an ai solution for restaurants to streamline your purchasing and inventory management processes, reducing potential expense losses.

Try to implement Expenditure Behavior Management (EBM) methodology to influence your progress and results. EBM is an awareness driven decision making practice in controlling business expenditures. This methodology helps you address your expenses proactively. It would let you understand how the decisions you make today affect current and future operations as a whole.

If you pay attention to your expenses, it doesn’t mean you are doing everything you can. Your business may experience constant loss from inefficient procedures that hadn’t been optimized before they became common behavioral practice. For instance, many restaurant owners have an old school approach to evaluating end-of-month reports, and then implement adjustments. This method fails to consider current cost controls already in place. Therefore this monthly ritual results only in forever gone profits, and puts you in an Expense Loss condition.

Expense Loss is the variance between money you unsystematically spend on product, services, or restaurant equipment and the achievable amount of money you can save by changing your spending behavior along with forward thinking procedures in place. Knowing the variance between the amount of money you are spending and the amount of money you can save, or the difference in how your decisions affect future outcomes, is paramount.

Cost Side and Lost Side spending behavior

A Cost Side Spending Behavior mentality is quite common among restaurant managers. When making decisions on spending money they ask themselves: ‘What will this cost me? ’ This approach is counterproductive to effective EBM because it makes people think that they make a one-time decision on an amount of money to spend that feels right. Further, it seems to them that there is no need to revisit this, especially if they are comfortable with their decision and the same expense is expected to come up again. Such spending behavior belongs to behavior patterns of a reactive type.

For example, following the cost side methodology, after you sign a contract with a vendor you no longer question the cost of the item or service provided by them no matter how much further reduction may be available in the market. You don’t ask yourself how much you may be losing in Expense Loss. Everyone is on board with the cost from the vendor and no further determinations are necessary. This behavior may continue until revenue drops below costs and a red flag goes up.

A Lost Side Spending Behavior mentality is the alternative. Managers who have this mentality see particular amounts of money as overspends reducing their profits. They take those overspends as a signal to be proactive next time this kind of expense occurs. Looking at expenses with a lost side mentality keeps managers informed and attentive to future decisions that will not follow the same outcome. Such spending behavior belongs to behavior patterns of a preemptive knowledge-based type.

For example, to start following the lost side methodology, you should look closely at the amounts lost from your purchasing and procedural decisions and sum them up. Look at your operations as a whole in service standards, cleanliness and appearance, purchases, receiving procedures, inventory management, or anything else your company deals with in its entirety. Try to see how each decision you made in each aspect of your business has contributed to your profit and where the Expense Loss condition exists.

Keep in mind that a procedural decision may include you having no procedure in place for a particular situation and how this lack of attention may be affecting expenses.

Expense loss you may have at the bar and at the kitchen

Waste management, over prepping, and not accounting for yields are just a few of the costly expenses associated with BOH operations. There are purchasing procedures, receiving procedures, and inventory management. Misunderstanding of these procedures can be extremely costly to a business.

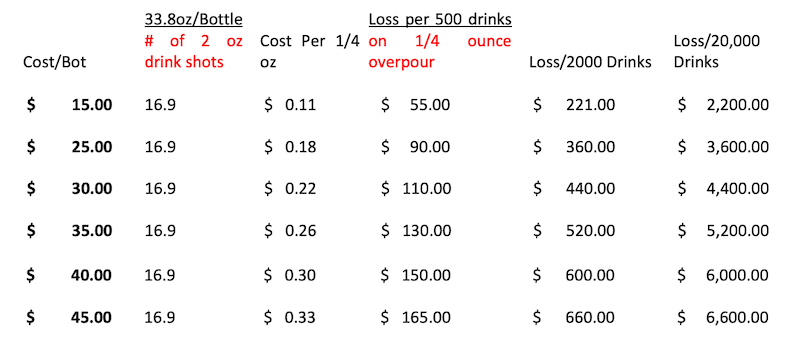

For example, running a bar, you need to know your Potential Pour Costs (PPC), Actual Pour Costs (APC), and understand recipe creation, costing, spillage, theft, etc. Consider that a 1⁄4 ounce over pour on one drink from a $30 bottle of alcohol is 22 cents each occurrence. Over an annual basis of 10,000 drinks poured with a 1⁄4 ounce over pour creates a $2,200 loss. Now add in the 2500 ¼ ounces lost in this scenario that could have made 416 more drinks using a 1.5 ounce pour at $8 a drink, (416 x $8) or $3,333, and you have a total Expense Loss of $5,533 for the year.

If you want to know how well your chef is managing expenses at the kitchen, you should follow any over prepping, waste, and the use of yield calculations management. Instead of relying only on food cost as a gauge, use the following three factors together to understand restaurant expenses for each day:

-

food cost percentage

-

daily menu mix

-

contribution to profit margin

After you consider those factors, share your insights with the rest of the team. If your staff doesn’t have this information, the chef cannot be fully to blame.

You can make a table to compare your Bottle Cost with Price Per Ounce and Loss to better understand the situation. Here is an example diagram that does not account for loss of revenue that results from over pouring, which is an additional thing to consider.

It’s difficult to make your restaurant expenses breakdown and get complete control over them as there are so many factors that contribute to your success or to your failure. Do your due diligence to learn or be trained about restaurant fixed costs and variable costs for a restaurant as much as possible. Having a grasp on your expenses can add significantly to your profits, and the more likelihood that you will succeed.